Just for fun, we picked up the Dec30 Puts in Cheesecake Factory (CAKE) at just before the close. I went short on the premise that "upscale casual dining" will only continue to suffer as the economy slows. JP Morgan also named CAKE its top short pick on Wednesday. It looks like the short play will pay off handsomely tomorrow. While CAKE management didn't have the you-know-whats to come clean during the conference call, the company issued a warning via press release that it would miss 4th quarter earnings and revenue estimates in the dark of night - at 9 p.m. eastern time! Can you believe that?? Given the fact that the company opted for subterfuge instead of warning four hours earlier during the conference call when after hours trading was taking place, we anticipate a wrathful reaction Friday morning.

Just for fun, we picked up the Dec30 Puts in Cheesecake Factory (CAKE) at just before the close. I went short on the premise that "upscale casual dining" will only continue to suffer as the economy slows. JP Morgan also named CAKE its top short pick on Wednesday. It looks like the short play will pay off handsomely tomorrow. While CAKE management didn't have the you-know-whats to come clean during the conference call, the company issued a warning via press release that it would miss 4th quarter earnings and revenue estimates in the dark of night - at 9 p.m. eastern time! Can you believe that?? Given the fact that the company opted for subterfuge instead of warning four hours earlier during the conference call when after hours trading was taking place, we anticipate a wrathful reaction Friday morning.

Thursday, November 30, 2006

CAKE - Cheesecake Factory

Just for fun, we picked up the Dec30 Puts in Cheesecake Factory (CAKE) at just before the close. I went short on the premise that "upscale casual dining" will only continue to suffer as the economy slows. JP Morgan also named CAKE its top short pick on Wednesday. It looks like the short play will pay off handsomely tomorrow. While CAKE management didn't have the you-know-whats to come clean during the conference call, the company issued a warning via press release that it would miss 4th quarter earnings and revenue estimates in the dark of night - at 9 p.m. eastern time! Can you believe that?? Given the fact that the company opted for subterfuge instead of warning four hours earlier during the conference call when after hours trading was taking place, we anticipate a wrathful reaction Friday morning.

LBO Chatter

I've been tied up today with home front related issues, but there is plenty of LBO chatter today causing shares of USG and Grace (GRA) to rally. As previously mentioned, time spreads are the way to go, or a quick in and out day trade on the calls. There's also takeover chatter surrounding Infospace (INSP). We haven't touched any of them mainly because of distractions with other things today.

Gold

What's not to like? The December contract is trading at $647.. next target is $650. In some respects, its unfortunate that this play has to occur because it's a commentary on many negative things - not the least of them, the dangerous world in which we live and the insane government spending of the last six years. Those two factors have largely been driving investors away from paper assets. As the American balance sheet continues to deteriorate and the dollar continues to weaken expect both new contract highs in gold and all time highs. Yes, I'm in the looney camp that sees gold going to at least $1,000+ in the next few years.

Chicago PMI

Wow... down to 49.9. This is a diffusion index, meaning any reading under 50 indicates CONTRACTION. Economists thought the index would rise to 54.5. Doh! This is certainly a negative surprise for the stock market and selling is already coming in. Plus, the weak PMI is on top of another weak jobless claims report - this time the filings went up 34,000. The March Euro contract is now closing in on 1.3300 as the dollar weakens on this data and gold is trading at its high of the day with the January contract already testing $650/oz. But don't worry - Helicopter Ben Bernanke told us the other day that the economy is just fine!

Wow... down to 49.9. This is a diffusion index, meaning any reading under 50 indicates CONTRACTION. Economists thought the index would rise to 54.5. Doh! This is certainly a negative surprise for the stock market and selling is already coming in. Plus, the weak PMI is on top of another weak jobless claims report - this time the filings went up 34,000. The March Euro contract is now closing in on 1.3300 as the dollar weakens on this data and gold is trading at its high of the day with the January contract already testing $650/oz. But don't worry - Helicopter Ben Bernanke told us the other day that the economy is just fine!{kind=link}

11/30/2006 Morning Market Comment

The dollar is attracting negative attention and is the the catalyst for a variety of other market moves this morning. The dollar index is down about a quarter of a point on the NYBOT at 83.21. How important is 83? Take a look here:

83 not only on this short term chart, but on multi year charts is a major support area. Traders are determined to see how low they can push the buck. This morning sterling is at a 14 yr high and the dollar is not to far against its recent low against the Euro. The dollar weakness has perked up gold futures again, with the metal flying past the $640 resistance this morning. We're back in with the January contract.

There's another barrage of economic data - every things from October core PCE, PCE deflator, personal spending, personal income and November Chicago PMI.

Stock futures are drifting higher on follow through to yesterday's momentum, but the effect of the weakening dollar and rising crude oil prices could put a damper on things as the day progresses.

Natural gas got to has high as $9.05 overnight, but has since pulled back by 14-cents - enough to stop us out. We use protective stops not only to protect against loss, but also to protect profits, and they've been big profits over the last week in the energy market for us. We may jump back in after the EIA data is released - expected to show a 24 bcf withdrawal. There is less technical resistance for crude and crude is now closing in on the $63/bbl level.

83 not only on this short term chart, but on multi year charts is a major support area. Traders are determined to see how low they can push the buck. This morning sterling is at a 14 yr high and the dollar is not to far against its recent low against the Euro. The dollar weakness has perked up gold futures again, with the metal flying past the $640 resistance this morning. We're back in with the January contract.

There's another barrage of economic data - every things from October core PCE, PCE deflator, personal spending, personal income and November Chicago PMI.

Stock futures are drifting higher on follow through to yesterday's momentum, but the effect of the weakening dollar and rising crude oil prices could put a damper on things as the day progresses.

Natural gas got to has high as $9.05 overnight, but has since pulled back by 14-cents - enough to stop us out. We use protective stops not only to protect against loss, but also to protect profits, and they've been big profits over the last week in the energy market for us. We may jump back in after the EIA data is released - expected to show a 24 bcf withdrawal. There is less technical resistance for crude and crude is now closing in on the $63/bbl level.

Wednesday, November 29, 2006

Pickens Sees Slim Pickins'

Boone Pickens is not one to pull punches. In this article,the famed Texas oilman warns of a coming supply problem. Yes, he's in the peak oil doom and gloom camp, but when a guy like this, who knows the oil industry inside and out, warns that the world will run out of oil in only 40 years - it pays to pay attention.

Boone Pickens is not one to pull punches. In this article,the famed Texas oilman warns of a coming supply problem. Yes, he's in the peak oil doom and gloom camp, but when a guy like this, who knows the oil industry inside and out, warns that the world will run out of oil in only 40 years - it pays to pay attention. HD - Home Depot - Is It a Takeover Candidate?? LOL

Street Noise: CNBC reported earlier today that private equity may be eyeing home improvement retailing behemoth Home Depot. That seems doubtful, at least if you look at the options. Take the December 37-1/2 calls. The offer has been trading about 10-cents BELOW theoretical value. This again highlights the danger of chasing after takeover rumors. More than 7000 of the HD Dec37-1/2 calls traded today as speculators went a chasin'. Oh, well... it's only money - right?

Street Noise: CNBC reported earlier today that private equity may be eyeing home improvement retailing behemoth Home Depot. That seems doubtful, at least if you look at the options. Take the December 37-1/2 calls. The offer has been trading about 10-cents BELOW theoretical value. This again highlights the danger of chasing after takeover rumors. More than 7000 of the HD Dec37-1/2 calls traded today as speculators went a chasin'. Oh, well... it's only money - right?

Midday Market Comment

Stocks are higher, but off the best levels of the day. It appears that crude oil above the $62/bbl level has partially offset the good news of stronger than previously reported GDP, pegged at a 2.2% annual rate in Q3. Housing data may also be moderating stock gains with a larger than expected 3.2% slide in new home sales reported this morning. We remain in the camp which believes housing market woes will be severe enough to cause a contraction in economic growth by mid-year next year. That, of course, flies in the face of the wisdom of the big crowd economists out there - not the least of them - Helicopter Ben Bernanke.

While stocks are off the best levels, this is a seasonally positive time for the market, volatility is slipping again, and so it is likely that the uptrend will continue at least through the month of December, before we get another batch of earnings reports in January. Especially close attention will need to be paid to the dollar, or really the Euro. A further sharp Euro advance could mean further stock market disruptions similar to the declines on Friday and Monday. For now, March Euro futures are down a quarter-percent with $1.3200 showing solid support. The dollar selling breather today is keeping the gold bulls on the defensive with the metal down $2/oz.

While stocks are off the best levels, this is a seasonally positive time for the market, volatility is slipping again, and so it is likely that the uptrend will continue at least through the month of December, before we get another batch of earnings reports in January. Especially close attention will need to be paid to the dollar, or really the Euro. A further sharp Euro advance could mean further stock market disruptions similar to the declines on Friday and Monday. For now, March Euro futures are down a quarter-percent with $1.3200 showing solid support. The dollar selling breather today is keeping the gold bulls on the defensive with the metal down $2/oz.

Natural Gas

No doubt, a combination of a surprise draw in the liquids and the forecast for colder than normal weather the first 10 days of December is sending natural gas to a more than 3% gain today. The strong move above the double top of $8.68 has prompted me to take a nearly $1/bbl profit in crude ($1,187 profit per crude futures contract) and roll into January natural gas e-mini contracts in search of a move toward the upper end of the September pivot at $8.97. The chart below shows this area approaching $9 will be a major area of resistance. +$9 would bring us back to the days when Amaranth was still alive.

DG - Dollar General

We warned recently that the speculation about Dollar General (DG) being taken out in an LBO sounded like "street noise" to us. Yesterday the rumor made it on to CNBC and the options and stock went flying. Today the stock is down 4%. No doubt, many went naked long on calls, which during times of rapidly rising implied volatility is one of the best ways to lose money; and that's exactly what's happening today. The only way to win at this type of game is to initiate what's known a time spread on the expectation that volatility will sink. For me, it's just not worth the trouble, especially with so many great futures plays available these days.

A Further Leg Up in the Energy Complex

There was a dip of 300k barrels in crude stocks, and a surprise 1 mln bbl draw in distillates, along with a 600k drop in gasoline stocks. Will the November pivot of $62 be taken out? Stay tuned.

F - Ford

Dow Jones newswire reports Ford is going to suspend its dividend. But even more amazing is this story.

RHAT - Redhat

Over 3,000 Dec17-1/2 calls have traded in the first half hour. The flyonthewall.com is reporting 'unconfirmed' takeover speculation. FWIW.

11/29/2006 Morning Market Comment

The stock market looks poised to build on yesterday's modest rebound following a night that featured a pullback for gold, once again from the very stubborn $640 resistance area, and a slight dollar dumping reprieve with March Euro futures showing a .3% dip.

There are going to be plenty of catalysts to enhance moves either way in various markets. Economic data will begin to flow with the 8:30 ET release of GDP, predicted to be revised to a 1.8% annual pace in Q3. The PCE inflation gauge is expected to remain steady at 2.3% and will be closely watched after yesterday's whine by the Fed chief that inflation remains uncomfortably high. Did anyone get the feeling that helicopter-Ben with his forecast for continued GDP growth next year is not connected with reality? At 10, October new home sales data will be released and a slight decline to 1,050k annual rate is expected. The Beige Book will be out midday.

We continue to find it hard to be overly bearish about the stock market at this point, and indicators like a decline in the put to call ratio and volatility index yesterday keep us in the mildy bullish camp. No doubt, the dollar slide, if it continues, will pose major risk to stock holdings; but the stock market is not showing signs - as of this time - of rolling over. We would not consider initiating a bearish play on the broader market until or unless the cash S&P 500 breaks below 1375; the SPY puts might be in order. All that we've seen out of the selling of Friday and Monday is a testing of the lower range of the recent upward channel in the cash S&P 500 which closed yesterday at 1386.

Energy continues to attract a bid, with WTI climbing to $61.50 overnight, but now back at the 61.15 mark. With colder than normal temps forecast for the first 10 days of December in the northeast and talk of another OPEC production cut, we will continue to hold our long position in crude futures to see if WTI can close above the Rita/Katrina trend line of $61.49.

Gold - We're staying away until the metal can close above $641.

Euro - We're on the sidelines until the Euro looks a bit less overbought.

There are going to be plenty of catalysts to enhance moves either way in various markets. Economic data will begin to flow with the 8:30 ET release of GDP, predicted to be revised to a 1.8% annual pace in Q3. The PCE inflation gauge is expected to remain steady at 2.3% and will be closely watched after yesterday's whine by the Fed chief that inflation remains uncomfortably high. Did anyone get the feeling that helicopter-Ben with his forecast for continued GDP growth next year is not connected with reality? At 10, October new home sales data will be released and a slight decline to 1,050k annual rate is expected. The Beige Book will be out midday.

We continue to find it hard to be overly bearish about the stock market at this point, and indicators like a decline in the put to call ratio and volatility index yesterday keep us in the mildy bullish camp. No doubt, the dollar slide, if it continues, will pose major risk to stock holdings; but the stock market is not showing signs - as of this time - of rolling over. We would not consider initiating a bearish play on the broader market until or unless the cash S&P 500 breaks below 1375; the SPY puts might be in order. All that we've seen out of the selling of Friday and Monday is a testing of the lower range of the recent upward channel in the cash S&P 500 which closed yesterday at 1386.

Energy continues to attract a bid, with WTI climbing to $61.50 overnight, but now back at the 61.15 mark. With colder than normal temps forecast for the first 10 days of December in the northeast and talk of another OPEC production cut, we will continue to hold our long position in crude futures to see if WTI can close above the Rita/Katrina trend line of $61.49.

Gold - We're staying away until the metal can close above $641.

Euro - We're on the sidelines until the Euro looks a bit less overbought.

Tuesday, November 28, 2006

The Currency 'Nuclear Option'

What's that old saying??? "All's fair in the world of fiat currencies." Yes, that's it. The Euro blasted above $1.30 last week, and I expect that in due course it will go to $1.35. Look for more fun and games ahead.

Gold

We picked a good exiting point the other night at just below $640/oz. for gold. Today the metal traded as low as the $632 level, then made a run back towards $640 only to hit a brick wall again. Rome wasn't build in a day, nor is a rebound for gold back to contract and then record highs. Clearly the chart below shows a very healthy rebound since October, with gold presently testing the lower bands of its recently bullish trading channel.

We're also going to initiate a position in Euro futures. I will post more on that separately.

We're also going to initiate a position in Euro futures. I will post more on that separately.

Chico's Puts

We picked up the CHS Dec22-1/2 puts at just before the close.

Earnings matched at 24c, but revs were light at $404 mln vs estimates of 417. November same store sales fell .4%. Shares have managed to nudge higher on relief the results weren't even worse than they were.

Earnings matched at 24c, but revs were light at $404 mln vs estimates of 417. November same store sales fell .4%. Shares have managed to nudge higher on relief the results weren't even worse than they were.

CHS - Chico's Earnings

Stock momentum is feeble ahead of this retailers results this evening, and put options volume is ahead of call volume in the December contracts by a 2 to 1 margin. in the new lingo of the younger generation... 'just sayin'. We have toyed with picking up the puts, but have made no final decision. The chart below shows that this thing is a 'gapper' and to the downside. Will history repeat itself?

Wind River Systems (WIND)

Put options in software optimization company Wind River have seen heavy activity. Over 4,000 Dec10 puts have traded today ahead of 12/5 earnings indicating large heading going on ahead of the results.

Today's Eco Data - Round #1

Durable goods spurring treasuries higher with a surprise drop...

Total Orders fell -8.3% (yikes), were down 1.7% ex transports and down 6.4% ex defense. So take the war machine out and you've got numbers that are a bit bearish for stocks though reaction to the data has only been modest thus far. The bulls can only hope there's an upward surprise in existing home sales numbers at 10.

Total Orders fell -8.3% (yikes), were down 1.7% ex transports and down 6.4% ex defense. So take the war machine out and you've got numbers that are a bit bearish for stocks though reaction to the data has only been modest thus far. The bulls can only hope there's an upward surprise in existing home sales numbers at 10.

11/28/06 Morning Market Comment

Markets calmed down overnight. While the dollar has been unable to recoup any its steep losses, the freefall did NOT accelerate overnight keeping gold in check (down less than $2) and U.S. stock futures little changed. Energy is holding on to a modest bid.

Investors are waiting for 8:30 ET Durable Goods and 10 a.m. existing home sales numbers and consumer confidence. 12:30 Helicopter-Ben will be speaking about the economic outlook and we'll hear from Chicago Fed President Moskow a little more than 4 hours later. Thus far, when Fed officials have spoken in recent weeks in tones to soothe dollar worries, they've gotten no respect from the markets.

Palm (PALM) cut its earnings forecast and pushed back the introductiuon of its TREO 750; PALM Is down 5%. Nokia (NOK) facing big network investment costs cut its margins forecast and is down 1%.

More on the day ahead after the 8:30 durables data.

Investors are waiting for 8:30 ET Durable Goods and 10 a.m. existing home sales numbers and consumer confidence. 12:30 Helicopter-Ben will be speaking about the economic outlook and we'll hear from Chicago Fed President Moskow a little more than 4 hours later. Thus far, when Fed officials have spoken in recent weeks in tones to soothe dollar worries, they've gotten no respect from the markets.

Palm (PALM) cut its earnings forecast and pushed back the introductiuon of its TREO 750; PALM Is down 5%. Nokia (NOK) facing big network investment costs cut its margins forecast and is down 1%.

More on the day ahead after the 8:30 durables data.

Risks of Recession On The Rise

Most economists feel, or more specifically, predict the U.S. will avoid a recession. Here's some interesting perspective by way of the San Francisco Fed.

Monday, November 27, 2006

December CBOT Gold

We've locked in a profit on the December 100 oz CBOT gold futures tonight. Our entry point was $632.70 and we exited at $639.60 for a gain of about $700 per contract. The $640 area remains a tough area of resistance even with the recent sharp dollar weakness. With no major support until the $633 level and tough resistance at $640, along with an RSI above 70 it was time to take a profit. IF gold can break above $642 in the near term, we would be buyers again with an objective of seeing gold recapture $650. Longer term, we have no doubt that gold is poised to rally strongly.

An UNeventful Day In Some Respects

Sure, the Dow fell nearly 160 points today, but much of the drop was accomplished fairly early on in the session. Volume by late afternoon at both the Big Board and the Nasdaq was lighter than normal. The market was at an impasse of sorts going into the close as the bulls opted not to do any bottom fishing and the bears decided not to push the market down even further - both sides kept in check by some very important economic data that's due tomorrow. Among the reports: durable goods orders, Conference Board consumer confidence and existing home sales.

A little before the close we sold our Apple (AAPL) Dec90 puts at a 58% gain and our Dec12 VIX calls for a gain of 25%. The price action in AAPL was lousy heading into the close and we anticipate further pressure on the stock, at least for the early part of tomorrow as a normal correction takes hold. We sold our put position today and locked in a nice gain knowing full well that AAPL is a market darling with almost a cult like following. Longer term negative bets against AAPL have proven fatal to many, but it was worth a quick downward nibble today.

A little before the close we sold our Apple (AAPL) Dec90 puts at a 58% gain and our Dec12 VIX calls for a gain of 25%. The price action in AAPL was lousy heading into the close and we anticipate further pressure on the stock, at least for the early part of tomorrow as a normal correction takes hold. We sold our put position today and locked in a nice gain knowing full well that AAPL is a market darling with almost a cult like following. Longer term negative bets against AAPL have proven fatal to many, but it was worth a quick downward nibble today.

Dell, Yahoo and EMC are Takeover Targets?

Street noise??? Private equity is "kicking some tires" according to Redherring.com. I'll believe it when it happens.

Mid Afternoon Market Comment

For all the reasons outlined this morning, the stock market is lower.

We initiated a put position in Apple (AAPL) earlier this morning and are presently sitting on a gain of about 50%. We stand at the ready to sell before the close. I have nothing against Apple per se, it will likely perform well going into earnings, but following its huge run (with that tell tale parabolic look on the chart), it should come as no surprise that it would run into a bout of profit taking especially on a down day for the overall market. At some point soon, the stock will likely cross the $100 mark, but not before some healthy consolidation.

Here's a 5 day Apple chart... classic double-top.

IF there is a final hour scamble in the overall market for the exits ahead of economic data this week, the $89.00 level could be tested today.

IF there is a final hour scamble in the overall market for the exits ahead of economic data this week, the $89.00 level could be tested today.

We also picked up calls tied to the Volatility Index (VIX) since the market has become, well... more volatile. The VIX Dec12 calls are also up around 40% at this point, and we may take a quick profit before closing.

Gold is trying to get back to the overnight highs, now back above the $641 level. We're still looking for a run toward $645 as the dollar continues to struggle.

We initiated a put position in Apple (AAPL) earlier this morning and are presently sitting on a gain of about 50%. We stand at the ready to sell before the close. I have nothing against Apple per se, it will likely perform well going into earnings, but following its huge run (with that tell tale parabolic look on the chart), it should come as no surprise that it would run into a bout of profit taking especially on a down day for the overall market. At some point soon, the stock will likely cross the $100 mark, but not before some healthy consolidation.

Here's a 5 day Apple chart... classic double-top.

IF there is a final hour scamble in the overall market for the exits ahead of economic data this week, the $89.00 level could be tested today.

IF there is a final hour scamble in the overall market for the exits ahead of economic data this week, the $89.00 level could be tested today.We also picked up calls tied to the Volatility Index (VIX) since the market has become, well... more volatile. The VIX Dec12 calls are also up around 40% at this point, and we may take a quick profit before closing.

Gold is trying to get back to the overnight highs, now back above the $641 level. We're still looking for a run toward $645 as the dollar continues to struggle.

Apple - Think Raises Target to $110

THNK raised its price target on Apple from $100 to $110 citing strong Black Friday sales. It is probably all true, and we've heard about brisk sales of the Ipod-shuffle. But we're not biting for a bullish play. With RSI over 75, the stock is looking over extended. We have picked up the Dec90 puts for a purely technical play with a short term stock price move to $90.

GOOG - we were finally stopped out of the Dec510 calls. We'll come back another day.

Natural Gas - I put a tight stop in this morning and it was taken out for what ended up being a small loss - in at $8.28 and out at $8.25 (a loss of about $150 per contract). I just didn't like its inability to hold above $8.35 and crude oil's inability to hold above $60.

GOOG - we were finally stopped out of the Dec510 calls. We'll come back another day.

Natural Gas - I put a tight stop in this morning and it was taken out for what ended up being a small loss - in at $8.28 and out at $8.25 (a loss of about $150 per contract). I just didn't like its inability to hold above $8.35 and crude oil's inability to hold above $60.

Retailing Winners and Losers

The analysts are starting to comment en masse about how retailers have faired.

BMUR has cut Aeropostale (ARO) to a SELL noting that the retailer has already resorted to 50% off sales to boost traffic.

Over at Wachovia, sales are exected to be above plan at AEOS and TJX. GPS and ANF appearing to have come up short.

One thing is certain, retailers as a group look droopy today and we'd be inclined to stay away both from long or short bets at this point.

BMUR has cut Aeropostale (ARO) to a SELL noting that the retailer has already resorted to 50% off sales to boost traffic.

Over at Wachovia, sales are exected to be above plan at AEOS and TJX. GPS and ANF appearing to have come up short.

One thing is certain, retailers as a group look droopy today and we'd be inclined to stay away both from long or short bets at this point.

11/27/06 Morning Market Comment

Front and center this morning is the dollar. After a slide that caught most everyone off guard during what was supposed to be a quiet holiday trading week last week, the greenback regained only a little lost ground overnight, but the Euro remains above $1.31.

The biggest problem for the buck is expectations the housing bust on this side of the Atlantic will slow the U.S. economy enough to force Helicopter-Ben and the gang at the Fed to cut interest rates early next year, while the ECB lifts rates further to cool Euroland economic growth. That would tilt money flows more in the direction of European assets. Last weeks comments by a VP, ok really THE VP at the People Bank of China, are also a burgeoning and negative reality. Remember, no Central Bank is going to admit to ‘selling’ dollars. They merely have to wink, insinuate, or just blurt out their desire to load up on less U.S. treasuries through ‘diversification’ – and voila, that’s enough to pressure the greenback. With our current account deficit what it is, overseas investors like the Peoples Bank are needed to buy as much U.S. paper as possible to fund the American debt fixation.

The dip in the dollar gave gold a boost overnight, but the metal has since moved back to about unchanged to a bit lower as traders await further dollar cues. The $640 area remains a major area of resistance. We continue to hold the December gold contract.

A plethora of economic data this week will play a big role to either enhance bearish dollar sentiment through weak data, or providing fuel for a relief rally on stronger data. A barrage of numbers are on the way: durable goods (+5%), consumer confidence (106.4), October existing home sales (6.2 mln), revised GDP (1.8%), jobless claims (315k), consumer spending (.1%), Chicago PMI (55), construction spending (unch), and November ISM (52.2).

Stock futures are soft as energy prices move higher. There's speculation that the OPECers will resort to another production cut to keep the price of crude supported. Colder weather is forecast in the northern tier of states by the end of the week. Our trade in natural gas is doing quite nicely this morning. Wal Mart with its forecast over the weekend of a slight decline in same store sales this month is also a negative on sentiment this morning. Wal Mart is down about 1% and a host of others are also trading lower. We were up in Bennington, VT over the weekend and paid a visit to a WMT store on Friday evening, and it was quiet with plenty of 32" and 42" HDTVs sitting at the front of the store.

GOOG is down another $4 in pre-market and we won't be surprised if we get stopped out this morning, but through other options and futures trades, the speculative/trading portfolio is up 54% over the past week, so we'll take the loss in GOOG and move on IF that's what happens this morning. A disciplined approach with respect to trading anything is essential but especially with leveraged assets likes options and futures. This means a stop loss level must be determined at the time of trade and the loss taken if the stop is hit.

GM shares are up 2-cents, but the longer term trend doesn't look good. The Journal devotes ink ink this morning to the travails of the auto industry with no end in sight thanks in part to the housing bust.

The Heard on the Street column (by subscription) of the Wall Street Journal takes aim at makers of drug coated stents: Johnson & Johnson (JNJ), Boston Scientific (BSX) and Abbott Laboratories (ABT). The column says the FDA will be holding safety hearings next month, something that is spooking investors as the hearings get closer. The stents have been increasingly blamed for causing heart attacks due to heightened risk of blood clots.

The biggest problem for the buck is expectations the housing bust on this side of the Atlantic will slow the U.S. economy enough to force Helicopter-Ben and the gang at the Fed to cut interest rates early next year, while the ECB lifts rates further to cool Euroland economic growth. That would tilt money flows more in the direction of European assets. Last weeks comments by a VP, ok really THE VP at the People Bank of China, are also a burgeoning and negative reality. Remember, no Central Bank is going to admit to ‘selling’ dollars. They merely have to wink, insinuate, or just blurt out their desire to load up on less U.S. treasuries through ‘diversification’ – and voila, that’s enough to pressure the greenback. With our current account deficit what it is, overseas investors like the Peoples Bank are needed to buy as much U.S. paper as possible to fund the American debt fixation.

The dip in the dollar gave gold a boost overnight, but the metal has since moved back to about unchanged to a bit lower as traders await further dollar cues. The $640 area remains a major area of resistance. We continue to hold the December gold contract.

A plethora of economic data this week will play a big role to either enhance bearish dollar sentiment through weak data, or providing fuel for a relief rally on stronger data. A barrage of numbers are on the way: durable goods (+5%), consumer confidence (106.4), October existing home sales (6.2 mln), revised GDP (1.8%), jobless claims (315k), consumer spending (.1%), Chicago PMI (55), construction spending (unch), and November ISM (52.2).

Stock futures are soft as energy prices move higher. There's speculation that the OPECers will resort to another production cut to keep the price of crude supported. Colder weather is forecast in the northern tier of states by the end of the week. Our trade in natural gas is doing quite nicely this morning. Wal Mart with its forecast over the weekend of a slight decline in same store sales this month is also a negative on sentiment this morning. Wal Mart is down about 1% and a host of others are also trading lower. We were up in Bennington, VT over the weekend and paid a visit to a WMT store on Friday evening, and it was quiet with plenty of 32" and 42" HDTVs sitting at the front of the store.

GOOG is down another $4 in pre-market and we won't be surprised if we get stopped out this morning, but through other options and futures trades, the speculative/trading portfolio is up 54% over the past week, so we'll take the loss in GOOG and move on IF that's what happens this morning. A disciplined approach with respect to trading anything is essential but especially with leveraged assets likes options and futures. This means a stop loss level must be determined at the time of trade and the loss taken if the stop is hit.

GM shares are up 2-cents, but the longer term trend doesn't look good. The Journal devotes ink ink this morning to the travails of the auto industry with no end in sight thanks in part to the housing bust.

The Heard on the Street column (by subscription) of the Wall Street Journal takes aim at makers of drug coated stents: Johnson & Johnson (JNJ), Boston Scientific (BSX) and Abbott Laboratories (ABT). The column says the FDA will be holding safety hearings next month, something that is spooking investors as the hearings get closer. The stents have been increasingly blamed for causing heart attacks due to heightened risk of blood clots.

Sunday, November 26, 2006

December CBOT Gold Update

We continue to hold a long position in the December CBOT 100 ounce gold futures contracts. Tonight the metal is trading above the $640 level as the dollar is falling again against the Yen and Euro. I like to take a very disciplined approach where profits are concerned. IF gold can move to resistance at $645, I will begin to cut my stake into that strength. I'll have further comment on the dollar and its impact on other markets before the open tomorrow.

Thanks For Stopping By!

I started this blog just a week ago. The counter below, which tracks unique visitors and not hits, has registered 2000 visitors in just the first week! Thanks for stopping in!

Jan Natural Gas - e-minNY

The heating season as been a balmy one thus far, but with a major cold shot set to move into the northeast next weekend, we see a brief weather related play in natural gas and have picked up the January e-mini futures contracts. The colder forecast for later this week may grease the way up to the $8.44 area and then into the $8.55 range. I will likely hold only for a few days since longer range forecasts for December by many pro mets who I follow are calling for transient cold snaps intermixed with warmer than normal temps. Many of these mets believe true winter cold won't lock in until the end of December.

As of Friday's close we were still holding on to our GOOG Dec510 calls. Maybe Monday will be the day we get stopped out. This isn't the first time that Barron's has given the stock a big thumbs down, but this article may be what does the trick.

Friday, November 24, 2006

December CBOT Gold

Gold ran into a brick wall at the $640 level, but the retreat from that mark has been modest with gold holding on to a gain of over $9. Our contingent sell order is pegged at $634/oz to lock in gains if the price fizzles, but I expect that we'll end up holding the CBOT December contracts through the weekend given today's strong price action and volume.

Neurochem (NMRX)

This is one to keep on the radar, Neurochem Inc (NMRX). Shares of NMRX have been bid up recently as investors anticipate fresh news. Streetinsider.com recently cited an analyst at JEFF as saying, "upcoming action on Kiacta (potentially by end of 2006, with class 1 review) could cause significant volatility in the shares." Results from the first phase 3 study of NRMX's Alzhemed-tramiprosate for the treatment of Alzheimer's disease is expected in the spring of 2007."

Getting my attention is the May options volatility which has surged to 133! Tramiprostate may eventually offer some hope to patients with mild to moderate Alzheimers disease. For now, it's an expensive lottery ticket in the options world, but a development worth watching. The options market has certainlyu taken notice.

Getting my attention is the May options volatility which has surged to 133! Tramiprostate may eventually offer some hope to patients with mild to moderate Alzheimers disease. For now, it's an expensive lottery ticket in the options world, but a development worth watching. The options market has certainlyu taken notice.

11/24/06 Morning Market Comment

While the collective American waistline expanded yesterday, blood flowed in the streets of Baghdad as the civil war in Iraq deepened. The worst sectarian violence to date in the Iraq war happened ahead of a scheduled three way weekend summit in Teheran between the Presidents of Iraq, Syria and Iran to discuss the security situation in Iraq and its regional implications. No doubt, the Sunni insurgents and foreign Jihadists are throwing everything they have at further destabilization ahead of the meeting; and no doubt the violence will continue.

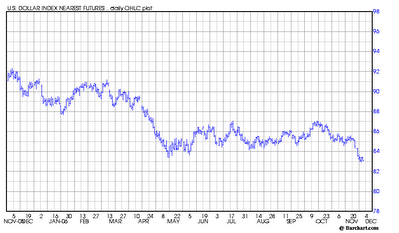

The dollar, in the meantime, continued to fall against the Yen and Euro on concerns the U.S. economy is slowing. The dollar woes gained a head of steam earlier this week following a larger than expected rise in jobless claims. Indeed, the dollar index (DXY) chart is looking very ugly:

Demand for the metal by way of the streetTRACKS gold ETF (GLD) has been so strong that the streetTracks gold holding has vaulted past 418 tons! We realize that buyers of streetTracks have been well supplied lately by Central Bank gold selling, but with a declining dollar, our confidence is growing that gold will make a run back toward the $680 level over the course of the next three months as the picture sours further for the buck.

One other gold note: CBOT electronic gold is trading today while COMEX is closed... that's a first and isn't it ironic that this first is happening on a day $10 up day for gold.

While we very much like the chart condition of Google (GOOG), if we get stopped out at $500 in a weak stock market today, so be it. We can always come back another day to pick up the GOOG Dec510 calls. GOOG is down over $3 bucks in the early going.

The dollar, in the meantime, continued to fall against the Yen and Euro on concerns the U.S. economy is slowing. The dollar woes gained a head of steam earlier this week following a larger than expected rise in jobless claims. Indeed, the dollar index (DXY) chart is looking very ugly:

The Euro surged to $1.30 for the first time since April 2005. There is also speculation that the ECB will continue to lift interest rates next year; that narrows the differential between the Euro and the buck, making the Euro look more appealing. The premium on U.S. government bond yields has also narrowed to the lowest level in about a 1-1/2 years further attracting investors into Euroland assets.

Quite frankly, the dollar's slide over the last week has almost been 'disorderly' and it's spooking the stock market. The only hope for the bulls is that thin holiday trading has exacerbated the dollar's decline and that there will be a rebound attempt in earnest when normal trading resumes next week. As the bloody debacle in Iraq gets worse and the dollar slides, the stock market is poised to break the positive Thanksgiving week tradition and not only open lower this morning, but potentially end lower for the week if it doesn't bounce off of this morning's lows.

Last night we picked up a position in the 100 oz. CBOT December gold contract (ZGZ6) in response to the recent dollar breakdown (a weaker dollar can spur inflation since it makes overseas goods more expensive). Each 10-cent move in gold translates into a $10 move in each contract's value, so we're sitting on a substantial gain with a $10 rise in the price of the metal this morning. $640 on the chart beckons again, but it will be a tough resistance area. The intraday technicals will need to be looked at carefully today to determine if I let the position ride through the weekend, or if I sell before the end of the day today to lock in gains. This may be the day we break $640, but then $645 stands as a roadblock. Stay tuned.

Demand for the metal by way of the streetTRACKS gold ETF (GLD) has been so strong that the streetTracks gold holding has vaulted past 418 tons! We realize that buyers of streetTracks have been well supplied lately by Central Bank gold selling, but with a declining dollar, our confidence is growing that gold will make a run back toward the $680 level over the course of the next three months as the picture sours further for the buck.

One other gold note: CBOT electronic gold is trading today while COMEX is closed... that's a first and isn't it ironic that this first is happening on a day $10 up day for gold.

While we very much like the chart condition of Google (GOOG), if we get stopped out at $500 in a weak stock market today, so be it. We can always come back another day to pick up the GOOG Dec510 calls. GOOG is down over $3 bucks in the early going.

Thursday, November 23, 2006

Gold Has Our Attention Again

We've picked up a long position in the December gold contract (ZGZ6) tonight. Softness in the dollar (DXY) has a lot to do with this decision. Further analysis in the morning. Incidentally, while the COMEX is closed tomorrow, the electronic CBOT gold contract starts trading... quite a coup by the CBOT.

Which Retailing Stock Should I Buy?

Everyone and his brother is wondering which consumer retailer stocks will outperform this holiday season. From a 'buy and hold' standpoint, I think that’s the wrong approach to take since it looks like the easy money has been made in a number of retailing names. Wal Mart's aggressive stance on pricing to regain lost traffic is putting everyone with similar merchandise (and that is literally almost everyone else) on the defensive. By quoting positive analyst comments, TheStreet.com ("Retailers Ready For the Spotlight") makes an argument for names like JC Penny (JCP), Target (TGT) and Nordstrom (JWN), but as usual the mainstream media is always a day late and dollar short. As an example, JCP has had great success in growing same store sales this year and there has been a commensurate rise in its share price: a run from the mid-50’s at the start of the year to the big 1998 highs of $80+. The JCP chart is incredible (perhaps argues for more of a possible stock split play), but it shows that theStreet.com has chosen to quote pundits who are pretty much endorsing a risky “buy high and sell higher” strategy.

While there may be plenty of momentum left to enable JCP to break historic resistance and make a run for the $100 mark, for me, every $1 made above that resistance would have been a dollar made with worry attached to it which is just not worth it.

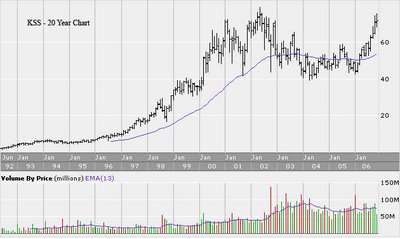

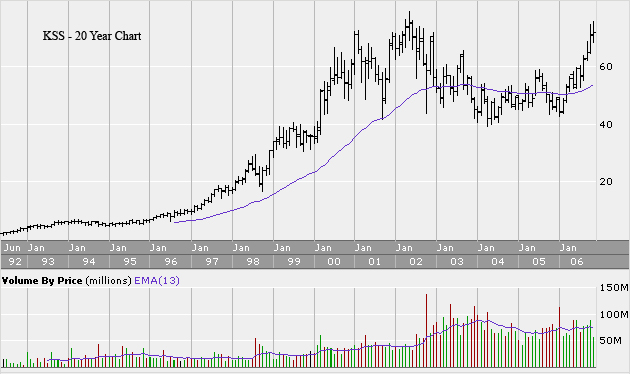

The 20 year chart for KSS shows the same problem of bumping up against major, multi-year resistance:

KSS, by the way, was one of the few retail laggards on Wednesday, falling by more than 1%. Money also rotated out of ANN, CBK, CWTR (big earnings miss), CHS and BDOG. Sears Holdings (SHLD) was the biggest winner Wednesday with a gain of almost 3%. I will have more on SHLD in a separate post.

The chart of Nordstrom shows a similar pattern of amazing returns and begs the question of, “why jump into these names now??”:

I have no doubt that with services like TheStreet.com touting these stocks, the crowd will jump in, but I’m not comfortable following the lemmings… err, the crowd. Sure, names like JCP, JWN, KSS could be seen as positive-trend-is-your-friend plays, and that there’s always the chance that the season will surprise to the upside (consumers are a clever bunch when it comes to finding extra spending money); but I’m going to keep the powder dry where the major retailers are concerned. I will revisit this stance when I see the same store sales data for November next week.

While there may be plenty of momentum left to enable JCP to break historic resistance and make a run for the $100 mark, for me, every $1 made above that resistance would have been a dollar made with worry attached to it which is just not worth it.

The 20 year chart for KSS shows the same problem of bumping up against major, multi-year resistance:

KSS, by the way, was one of the few retail laggards on Wednesday, falling by more than 1%. Money also rotated out of ANN, CBK, CWTR (big earnings miss), CHS and BDOG. Sears Holdings (SHLD) was the biggest winner Wednesday with a gain of almost 3%. I will have more on SHLD in a separate post.

The chart of Nordstrom shows a similar pattern of amazing returns and begs the question of, “why jump into these names now??”:

I have no doubt that with services like TheStreet.com touting these stocks, the crowd will jump in, but I’m not comfortable following the lemmings… err, the crowd. Sure, names like JCP, JWN, KSS could be seen as positive-trend-is-your-friend plays, and that there’s always the chance that the season will surprise to the upside (consumers are a clever bunch when it comes to finding extra spending money); but I’m going to keep the powder dry where the major retailers are concerned. I will revisit this stance when I see the same store sales data for November next week.

There is no doubt about the momentum surrounding some of the names in the space, and from an options standpoint, we're going to jump in for short term plays (as we do, I will publish the plays on the blog).

Some Food For Thought

Dear Readers,

Dear Readers,U.S. markets are closed today. Aside from tomorrow’s scheduled half day of trading in the stock market, most U.S. markets will remain closed until Monday morning. We get to enjoy a long holiday weekend courtesy of President Abraham Lincoln who in 1863 set aside the last Thursday of November “as a day of Thanksgiving and Praise to our beneficent Father who dwelleth in the Heavens.” FDR had Congress change Thanksgiving to the present 4th Thursday of November. For the entire Lincoln Thanksgiving proclamation Click here.

Little did Lincoln realize, but his proclamation would spur the Swanson brothers to invent the TV Dinner 90 years later. The true tale is told here at this amazing link. But let's hope you're having home roasted turkey today.

Happy Thanksgiving!

Happy Thanksgiving!

Wednesday, November 22, 2006

Brocade December8 Calls

For the purposes of options speculation, we've accomplished what we set out to do. We've sold our Dec8 BRCD calls for a gain of 86%. Any near term dip in BRCD following large gains in the stock would present a great longer term opportunity.

GOOG December Calls

We jumped in and added further to our Dec510 GOOG calls earlier in the session. We may do the same if there is further low-volume weakness on Friday. (See comments earlier concerning EBITDA valuation). We see no reason not to believe that the breakout won't continue next week when the crowd gets back to business after the long holiday weekend. Technical models that we favor, including MACD, RSI and Chalkin, indicate there is room for further upside. This is also a seasonally positive time of the year for shares of GOOG.

Kirk and MGM

There's never a dull day for 90 year old billionaire investor Kirk Kerkorian. In addition to trimming his massive GM stake, his Tracinda Corp Tracinda is planning a cash tender for up to 15 million shares of MGM Mirage (MGM) at a price of $55. MGM is up 10% at just above $54. Could there be more upside? At least one firm is very bullishing. STFL today lifted its price target on MGM from $50 to $65.

Dollar General - Takeover Chatter

More Street noise: This time around LBO takeover talk has helped to boost shares of Dollar General (DG) by over 7% today. Volatility is fairly low and trading is lackluster in DG options.

FCX and BHP

The BHP takeover chatter persists, pushing shares of Freeport (FCX) to a gain of more than $3 in the first hour of trading. Options prices are very expensive with the December 60's trading at $3.70 bid... the Dec65s at $1.60 bid. Anything can happen in the merger-hot mining industry, and for now the market is putting some credence into the takeover speculation. FCX would owe a hefty $375 mln breakup fee to PD if its buyout goes south. The most active of the December PD puts is the Dec110s; not heavy volume at 786 contracts, but an indication that some are hedging, or perhaps gambling that the PD deal won't make it.

11/23/06 Morning Market Comment

After another dull regular trading session yesterday some fireworks erupted after hours. The biggest development was Dell's "preliminary" profit coming in 6c ahead of expectations. Dell is up 9% this morning. DBAB raised its Dell target to $32 from $28 a share. FACT maintains a NEUTRAL rating, but has a positive bias; First Albany encouraged by pricing discipline and stronger server business. UBSW raised its estimates and price target to $27. BEST upgraded Dell to OUTPERFORM from PEER PERFORM with a target of $35. MP ups its target from $20 to $30 thanks to improved margins.

Another winner on the earnings gravy train: Brocade is trading over 6% higher at over $9/shr. PACS has raised its target to $12 from $10 and keeps BRCD as a "top pick". Brocade has been upgraded at NEED to BUY from HOLD with a $10.50 price target. Needham says it is more positive about the company's outlook and execution after yesterday's storng results.

J Crew (JCG) is up better than 8% on strong earnings; CWTR on the downside after earnings, lower by 4-1/2%

Google (GOOG) remains a market darling, up another $3 in pre market activity. JEFF notes that option implied volatility on GOOG is only 29, at the low end of its historical range. JEFF also notes that even above $500, GOOG is trading at 22x fiscal-07 EDITDA also within its historical range, though certainly not cheap.

The Heard On The Street column of the Wall Street Jounral devotes ink this morning to takeover speculation. It's not IF, but WHO? The column says Sprint-Nextel (S), Hilton (HLT), Lennar (LEN), Ryland (RYL), D.R. Horton (DHI) and ServiceMaster (SV) could be ripe for the picking. But the columns cautions, “But investors shouldn't get carried away betting on possible takeovers. Not only are they tough to predict, these deals also are somewhat less lucrative than they once were. The average premium paid over market prices for shares of companies subject to an acquisition bid this year is 17%, down from 25% in 2000, according to Thomson Financial.” Details here (subscription required): http://online.wsj.com/article/heard_on_the_street.html?mod=djemheard.

Speaking of takeover talk, US Steel (X) remained strong yesterday… even Nabors (NBR) held on to a bid despite a spokesman, on Monday, saying takeover rumors were “unfounded”. There is also over the top speculation that BHP could be mulling a takeover of Freeport McMoRan (FCX), though Freeport has agreed to acquire Phelps Dodged (PD). It’s over the top, but nowadays you just never know.

Stock futures are higher across the board boosted by strong earnings and ongoing takeover speculation. As the equity only put to call ratio and volatility measures continue to slide there's certainly a whiff of an overbought and complacent condition in the market, but the picture still remains fairly bullish.

NYMEX floor trading is closed for the rest of the week. EIA data will be out later in the morning. Analysts are guessing crude stocks will rise by 700k/bbl and drops of 750k in mogas and by 1.1 mln/bbs in distillates. EIA nat gas inventory data will also be out a day early, and a withdrawal of 3 to 7 Bcf is expected. In electronic trading this morning, Jan WTI is down 24-cents. Cold is trying again, up $1.80 at the $630 mark.

Another winner on the earnings gravy train: Brocade is trading over 6% higher at over $9/shr. PACS has raised its target to $12 from $10 and keeps BRCD as a "top pick". Brocade has been upgraded at NEED to BUY from HOLD with a $10.50 price target. Needham says it is more positive about the company's outlook and execution after yesterday's storng results.

J Crew (JCG) is up better than 8% on strong earnings; CWTR on the downside after earnings, lower by 4-1/2%

Google (GOOG) remains a market darling, up another $3 in pre market activity. JEFF notes that option implied volatility on GOOG is only 29, at the low end of its historical range. JEFF also notes that even above $500, GOOG is trading at 22x fiscal-07 EDITDA also within its historical range, though certainly not cheap.

The Heard On The Street column of the Wall Street Jounral devotes ink this morning to takeover speculation. It's not IF, but WHO? The column says Sprint-Nextel (S), Hilton (HLT), Lennar (LEN), Ryland (RYL), D.R. Horton (DHI) and ServiceMaster (SV) could be ripe for the picking. But the columns cautions, “But investors shouldn't get carried away betting on possible takeovers. Not only are they tough to predict, these deals also are somewhat less lucrative than they once were. The average premium paid over market prices for shares of companies subject to an acquisition bid this year is 17%, down from 25% in 2000, according to Thomson Financial.” Details here (subscription required): http://online.wsj.com/article/heard_on_the_street.html?mod=djemheard.

Speaking of takeover talk, US Steel (X) remained strong yesterday… even Nabors (NBR) held on to a bid despite a spokesman, on Monday, saying takeover rumors were “unfounded”. There is also over the top speculation that BHP could be mulling a takeover of Freeport McMoRan (FCX), though Freeport has agreed to acquire Phelps Dodged (PD). It’s over the top, but nowadays you just never know.

Stock futures are higher across the board boosted by strong earnings and ongoing takeover speculation. As the equity only put to call ratio and volatility measures continue to slide there's certainly a whiff of an overbought and complacent condition in the market, but the picture still remains fairly bullish.

NYMEX floor trading is closed for the rest of the week. EIA data will be out later in the morning. Analysts are guessing crude stocks will rise by 700k/bbl and drops of 750k in mogas and by 1.1 mln/bbs in distillates. EIA nat gas inventory data will also be out a day early, and a withdrawal of 3 to 7 Bcf is expected. In electronic trading this morning, Jan WTI is down 24-cents. Cold is trying again, up $1.80 at the $630 mark.

Tuesday, November 21, 2006

Google Insiders Dumping LESS Shares

Interesting read in Barron's Online's "Inside Scoop" that insiders at the Internet giant are not selling their shares with the same fervency of the past. Cutting to the chase, the Barron's report says insider sales have totaled about 9-1/2 mln shares in the open market in 2006; that's down from sales of 16 mln shares in 2005. The Barron's write-up quotes Ben Silverman, a director of research at InsiderScore.com as saying with Google executing well "investor appetite hasn't waned." Further details (subscription required): http://online.barrons.com/article/SB116406803894128905.html?mod=9_0002_b_online_exclusives_left

Trading the Thanksgiving Market

Here's a wrap up of today's market courtesy of our favorite financial site, WSJ.Com. In this write up, some interesting perspective on how Thanksgiving weeks are generally UP weeks for the U.S. stock market (subscription required): http://online.wsj.com/page/2_0064.html?mod=2_0064

Here's a wrap up of today's market courtesy of our favorite financial site, WSJ.Com. In this write up, some interesting perspective on how Thanksgiving weeks are generally UP weeks for the U.S. stock market (subscription required): http://online.wsj.com/page/2_0064.html?mod=2_0064

Brocade (BRCD) Beat the Street Again

BRCD 4th quarter earnings amounted to 14c vs. consensus estimates of 12c. Revenue of $208.8 mln vs. consensus estimates of $203.51 mln. BRCD moved higher AH which should enable us to take a profit at some point tomorrow morning on the BRCD calls.

BRCD 4th quarter earnings amounted to 14c vs. consensus estimates of 12c. Revenue of $208.8 mln vs. consensus estimates of $203.51 mln. BRCD moved higher AH which should enable us to take a profit at some point tomorrow morning on the BRCD calls.Dell managed to beat by a big 6c a share and the stock has moved past the $27 level. As noted earlier, we stayed off to the sidelines this time around... better to be a chicken than a dead duck.

Another earnings winner this evening is J Crew (JCG) posted earnings of 27c, a full 6c above estimates.

Google (GOOG) finished just a touch below the highs of the day and we will continue to hold our December calls until the momentum either grinds to a halt, or we see a blow off near term top on volume of 12 mln shares or more. Today's volume totaled 8.4 mln.

Quick Crude Comment

We're going to continue to hold onto our long position in the Jan-emiNY QMF7 crude futures going into EIA inventory numbers tomorrow morning.

Brocade (BRCD)

Ahead of earnings we've picked up some of the BRCD Dec8 calls. Momentum is positive going into the earnings release tonight and we like that they've been able to exceed street estimates in recent quarters.

Interdigital Comm (IDCC)

Street Noise: The rumors are back that Qualcomm (QCOM) might buy IDCC. Until we see options volume in the in the money calls exceed open interest on a given day the IDCC rumors are just idle chatter to us.

Enzon (ENZN)

More than 50x the normal volume of ENZN Feb10 calls have traded today. The company is in the midst of a phase 1 trial of Oncaspar to assess its safety and use in the treatment of advanced solid tumors and lymphomas in combination with Gemzar(R). These Feb10s might be worth a shot since they are only trading at around .30-cents.

Dell - We're NOT In

We're staying off to the sidelines on Dell given the uncertainties over the Dell balance sheet amid the SEC investigation. An SEC probe is always a red flag in my book, BUT - and this is a big but - there are just too many unknowns to make an educated speculative decision on whether to go long or short. There is just no predicting what items like off balance sheet entities, exploding payables and tangible assets will look like. Dell certainly won't dare fudge anything since SEC is looking over their shoulder, but the company can use 'preliminary' numbers to reduce transparency and as a way to retroactively revise figures in the future. Dell can also use any number of tricks with respect to changes in deferrals of revenue recognition and expense capitalization to give a near term boost to its numbers.

The battle lines are certainly drawn. In the December options, 42k Dec 25 calls have traded vs volume of 18k puts. Open interest on the Dec25 calls also out numbers OI on the puts by 16k contracts. Given that implied volatility is about its long term average, both sides may get little satisfaction unless there is a huge surprise which is not factored into the pricing of the options.

The battle lines are certainly drawn. In the December options, 42k Dec 25 calls have traded vs volume of 18k puts. Open interest on the Dec25 calls also out numbers OI on the puts by 16k contracts. Given that implied volatility is about its long term average, both sides may get little satisfaction unless there is a huge surprise which is not factored into the pricing of the options.

Google Over $500 - We're In

I've been out, first to a breakfast meeting, then an appointment at the doctor, then to the famed Rockland Bakery to pick up some baked goods for Thanksgiving. But through the miracle of being able to surf the web via Motorola Q phone, I did pop an order in for GOOG 510 calls. Volume on shares of GOOG thus far is 5.4 mln shares; so we're content to hold until we see evidence of a buying climax, which for GOOG has usually meant volume above 10 mln shares. Our mental stop is 500.

Dell Computer (Dell)

Dell is indicated to open a skosh higher this morning ahead of its 'preliminary' results after the bell today. I will have more analysis a little later, but if HP reported great results recently and its stock went south, what direction will Dell's shares go after its expected lackluster results are released? There could be a sense of relief if guidance is provided with respect to the SEC investigation, but given that we know the other part of the equation - that HP, et al are cleaning Dell's clock - there doesn't seem to be much hope for the Dell bulls, some of whom have loaded up big time on Jan30 calls. More later.

11/21/06 Morning Market Comment

We enter another trading day with volatility near all time lows. Technically speaking the $VIX is at the lowest level in 13 years and the $VXO is at its lowest level since July of 2005. Given the extremely low level of the VIX a call play would seem to make sense and it's something we will look at later today. In the early going, there's a modest bid to stock futures; crude oil is firming up and gold is trying again with a gain of about $4/oz. There's a big platinum play going on this morning. Platinum hit a record in London on speculation a new investment fund for the metal will make it more accessible to investors, putting a squeeze on supply.

Shares of John Deere (DE) are down about 3%. While earnings beat street estimates, DE say's "equipment sales are projected to be roughly flat for the full year and increase approximately 5% for the 1st Q of 2007".

Among top-5 stocks/indexes with high put/call ratios yesterday:

Tyson (TSN), Consumer Discretionary (XLY), WW Grainger Inc (GWW) and Ameriprise Financial (AMP).

All in all, it's likely to be another less than magnamimous day on Wall Street, but as long as the bulls can keep the major indexes moving along that narrow upward channel we talked about yesterday, the case remains modestly bullish.

Shares of John Deere (DE) are down about 3%. While earnings beat street estimates, DE say's "equipment sales are projected to be roughly flat for the full year and increase approximately 5% for the 1st Q of 2007".

Among top-5 stocks/indexes with high put/call ratios yesterday:

Tyson (TSN), Consumer Discretionary (XLY), WW Grainger Inc (GWW) and Ameriprise Financial (AMP).

All in all, it's likely to be another less than magnamimous day on Wall Street, but as long as the bulls can keep the major indexes moving along that narrow upward channel we talked about yesterday, the case remains modestly bullish.

It's Time For... Faaaaamilllllyyyyyy Feuuuuuddddd

No wonder Sumner Redstone has no tolerance for actors who jump up and down on Oprah's couch. This guy has some big family problems on his has hands. Where's Richard Dawson when we need him most? (subscription required): http://online.wsj.com/article/SB116404249182028499.html?mod=home_whats_news_us

No wonder Sumner Redstone has no tolerance for actors who jump up and down on Oprah's couch. This guy has some big family problems on his has hands. Where's Richard Dawson when we need him most? (subscription required): http://online.wsj.com/article/SB116404249182028499.html?mod=home_whats_news_us

Monday, November 20, 2006

So, There Is Still A Little Decency Left

Newscorp is pulling both the O.J. Simpson "hypothetical" and its associated t.v. special: http://www.foxnews.com/story/0,2933,230838,00.html.

(by subscription): http://online.wsj.com/article/SB116405450775128696.html?mod=home_whats_news_us

This leads me to wonder why Newscorp thought it could get away with this in the first place. Could they really have been caught so off guard by the firestorm of criticism directed toward "If I Did It"? If so, they are a bunch of dolts - from Murdoch on down.

I also can't help but to wonder whether the entity that was paid the $3.5 mln by the Regan imprint of HarperCollins for the book gets to keep the $3 mln? Perhaps O.J. misses out on another 15 minutes of fame with his book being pulled, but his family, or whomever was going to reap the financial rewards of the book may still end up quite a bit wealthier.

And one other question, what happens to all of the copies of the book now sitting in warehouses? At least 200,000 copies had to have been printed for next week's release. If there ever was a good reason for a mass book burning, "If I Did It" would be it.

(by subscription): http://online.wsj.com/article/SB116405450775128696.html?mod=home_whats_news_us

This leads me to wonder why Newscorp thought it could get away with this in the first place. Could they really have been caught so off guard by the firestorm of criticism directed toward "If I Did It"? If so, they are a bunch of dolts - from Murdoch on down.

I also can't help but to wonder whether the entity that was paid the $3.5 mln by the Regan imprint of HarperCollins for the book gets to keep the $3 mln? Perhaps O.J. misses out on another 15 minutes of fame with his book being pulled, but his family, or whomever was going to reap the financial rewards of the book may still end up quite a bit wealthier.

And one other question, what happens to all of the copies of the book now sitting in warehouses? At least 200,000 copies had to have been printed for next week's release. If there ever was a good reason for a mass book burning, "If I Did It" would be it.

More Cracks In The Housing Market

This latest data is lagging, but ugly none-the-less: http://www.thestar.com/NASApp/cs/ContentServer?pagename=thestar/Layout/Article_Type1&c=Article&cid=1164019629316&call_pageid=968350072197&col=969048863851

But have no fear, your favorite economist more than likely thinks the worst is over for the housing bust (subscription required): http://online.wsj.com/article/SB116370236302025327.html?mod=djemalert

For reasons previously stated, I'm in the camp who believes housing won't bottom until 2008. Is there anyone who would seriously argue that economists as a group aren't a contrary indicator? LOL.

But have no fear, your favorite economist more than likely thinks the worst is over for the housing bust (subscription required): http://online.wsj.com/article/SB116370236302025327.html?mod=djemalert

For reasons previously stated, I'm in the camp who believes housing won't bottom until 2008. Is there anyone who would seriously argue that economists as a group aren't a contrary indicator? LOL.

GOOG and $500 - Not So Fast

True to form, Google got so close on Friday to hitting the $500 mark, but never made it. Past century mark experiences at 400, 300 and 200 have shown that leaping past century marks doesn't necessarily happen as fast the GOOG bulls would like. Today the stock is struggling, but down only about 1% on the day. The five day chart above cautions for a possible filling of last week's gap in the $489 area in the near term.

We briefly jumped into the frenzy surrounding Nabors (NBR), no sooner had we entered in with the purchase of the NBR Dec32-1/2 calls at an average of $1.43 that they flew to $2. At that point a spokesman said takeover speculation was unfounded. We ended up bouncing out at .90. OUCH.

X - U.S. Steel

Steel stocks roared out of the gate this morning. My 40 call position in the U.S. Steel (X) December 80 calls surged as well. I have sold the entire options position for a net 1 day gain of 83%.

11/20 Morning Comment

It's a merger Monday in a big way once again, with the $26 bln takeout of Phelps Dodge (PD) by Freeport (FCX), a $20 bln buyout of Equity Office Properties (EOP) by Blackstone and Nasdaq's (NDAQ) $5 bln bid for the London Stock Exchange.

Merger mania whether across transatlantic time zones with the Nasdaq bid, or in the merger-hot mining sector, or by way of the ongoing LBO's (more than $3 trillion worth this year) can only serve to support the stock market even as ominious housing meltdown storm clouds develop on the horizon. This chart of the S&P 500 illustrates a bullish upward channel - the 'trend remains your friend' - for now.

Merger mania whether across transatlantic time zones with the Nasdaq bid, or in the merger-hot mining sector, or by way of the ongoing LBO's (more than $3 trillion worth this year) can only serve to support the stock market even as ominious housing meltdown storm clouds develop on the horizon. This chart of the S&P 500 illustrates a bullish upward channel - the 'trend remains your friend' - for now.

Futures are on the soft side this morning, following a modestly positive Friday expiration. Put to call ratios remain low (though 2 mln Wynn calls that traded Friday on a dividend capture play have distorted the picture) and the VIX continues to flirt with all time lows. That low VIX isn't necessarily a good thing since it indicates dangerously low complacency that will eventually be resolved in probably a not so happy way for the bulls. PD in pre market trading is up $27 at $121, while FCX is down only $4. EOP is up by better than $3

Futures are on the soft side this morning, following a modestly positive Friday expiration. Put to call ratios remain low (though 2 mln Wynn calls that traded Friday on a dividend capture play have distorted the picture) and the VIX continues to flirt with all time lows. That low VIX isn't necessarily a good thing since it indicates dangerously low complacency that will eventually be resolved in probably a not so happy way for the bulls. PD in pre market trading is up $27 at $121, while FCX is down only $4. EOP is up by better than $3

.

My holding in X calls may benefit from another $2+ early rally in shares of U.S. Steel on steel industry merger speculation which is turning white hot. The catalyst for further upside in shares of steel today is the $2 bln takeover of Oregon Steel Mills by Russia's Evraz Group. Who's next? X, NUE, CHAP, STLD??

WTI is modestly lower, and this is where I will continue to focus the bulk of my trading activity this holiday shortened week. The large specs are now bullish for the first time since October, but even with the implied bullishness the December contract still went off the board at its lowest since the summer of 2005.

Gold is up about $2, but I continue to stay away until I see a further breakdown in the dollar and I become bullish on crude.

Sunday, November 19, 2006

More Pre-Monday Musings

Another big merger Monday is in the making, with over $40 bln in deals thus far:

In the ever merger-hot mining industry, Phelps Dodge (PD) is Freeport-McMoRan's (FCX) to have and to hold for the price of $25.9 bln in cash and stock. Phelps is being taken out at $126/shr vs its Friday closing price of $95. Trading in PD call options was moderate at about 9,000 contracts for the December strikes.

In another whopper of a deal, The Wall Street Journal reports Blackstone is set to annonce a takeover of Equity Office Properties (EOP) for $20 bln, or $48.50/sh. That's about a 10% premium to Friday's closing price. Call options trading in EOP was fairly quiet on Friday, with only about 600 December calls trading - 522 were the December 45s.

The ongoing activity of competitors gobbling each other up and private equity firms willing to pay decent premiums to take companies private continues to be a large factor in the 'bullish column' for investors to be mindful of.

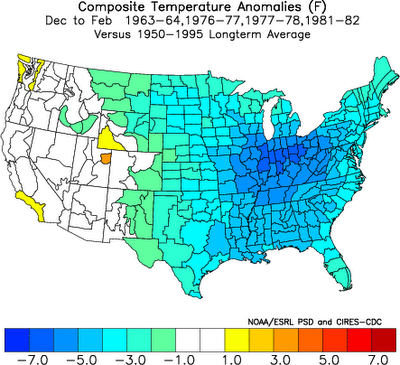

It's only 7 p.m. eastern time, but crude oil is off to a lower start with the Jan contract down a-half percent, or 29-cents/bbl. Natural Gas is down .8%. In the near term, there's more reason to be bearish than bullish - the chief factors being plentiful supply both in all strata of the barrel market and in underground natural gas storage; mild northeast temps relative to norms; and no immediate prospect of mushroom clouds being seen over the Middle East. So my bias and approach toward trading crude oil futures will be a continued bearish mindset, but being ever mindful of emergent, or nascent bullish factors like geopolitical events and a swing toward a colder direction for the winter season (at some point). Thus far, temps are looking great if you like it on the milder side. The operational GFS is predicting high temps in NYC to remain above 40f through December 3rd! This will continue to be a bearish influence on the energy markets. But here's something else to consider:

The above is a composite of how aggregate winters turned out following fall seasons with a mild/moderate El Nino: cold winters. This stuff isn't perfect, of course, but it's a reminder backed by past data that a surprise turn of events may occur to catch those off guard who are expecting another above average winter and the bearish impact on the energy markets to continue through the winter.

In the ever merger-hot mining industry, Phelps Dodge (PD) is Freeport-McMoRan's (FCX) to have and to hold for the price of $25.9 bln in cash and stock. Phelps is being taken out at $126/shr vs its Friday closing price of $95. Trading in PD call options was moderate at about 9,000 contracts for the December strikes.

In another whopper of a deal, The Wall Street Journal reports Blackstone is set to annonce a takeover of Equity Office Properties (EOP) for $20 bln, or $48.50/sh. That's about a 10% premium to Friday's closing price. Call options trading in EOP was fairly quiet on Friday, with only about 600 December calls trading - 522 were the December 45s.

The ongoing activity of competitors gobbling each other up and private equity firms willing to pay decent premiums to take companies private continues to be a large factor in the 'bullish column' for investors to be mindful of.

It's only 7 p.m. eastern time, but crude oil is off to a lower start with the Jan contract down a-half percent, or 29-cents/bbl. Natural Gas is down .8%. In the near term, there's more reason to be bearish than bullish - the chief factors being plentiful supply both in all strata of the barrel market and in underground natural gas storage; mild northeast temps relative to norms; and no immediate prospect of mushroom clouds being seen over the Middle East. So my bias and approach toward trading crude oil futures will be a continued bearish mindset, but being ever mindful of emergent, or nascent bullish factors like geopolitical events and a swing toward a colder direction for the winter season (at some point). Thus far, temps are looking great if you like it on the milder side. The operational GFS is predicting high temps in NYC to remain above 40f through December 3rd! This will continue to be a bearish influence on the energy markets. But here's something else to consider:

The above is a composite of how aggregate winters turned out following fall seasons with a mild/moderate El Nino: cold winters. This stuff isn't perfect, of course, but it's a reminder backed by past data that a surprise turn of events may occur to catch those off guard who are expecting another above average winter and the bearish impact on the energy markets to continue through the winter.

Saturday, November 18, 2006

Thanksgiving Week

Monday and Tuesday will be the only normal trading days of the week; by midday Wednesday much of the crowd will be clearing out of lower Manhattan in preparation for Thursday’s overdose of tryptophan also known as Thanksgiving Day. Trading resumes on Friday – retailer Black Friday – but the day after Thanksgiving is traditionally among the slowest trading days of the year since the market is only open a half day.